Comparable Company Analysis – Financial Ratios

Identifying good comparable companies is essential for building a robust valuation model. We earlier wrote about some of the nonfinancial aspects that you may want to consider when deciding on comparable. You can read about it here. In this post, we’re talking about the key financial ratios that you may want to analyze to understand the quality of your comparable selection.

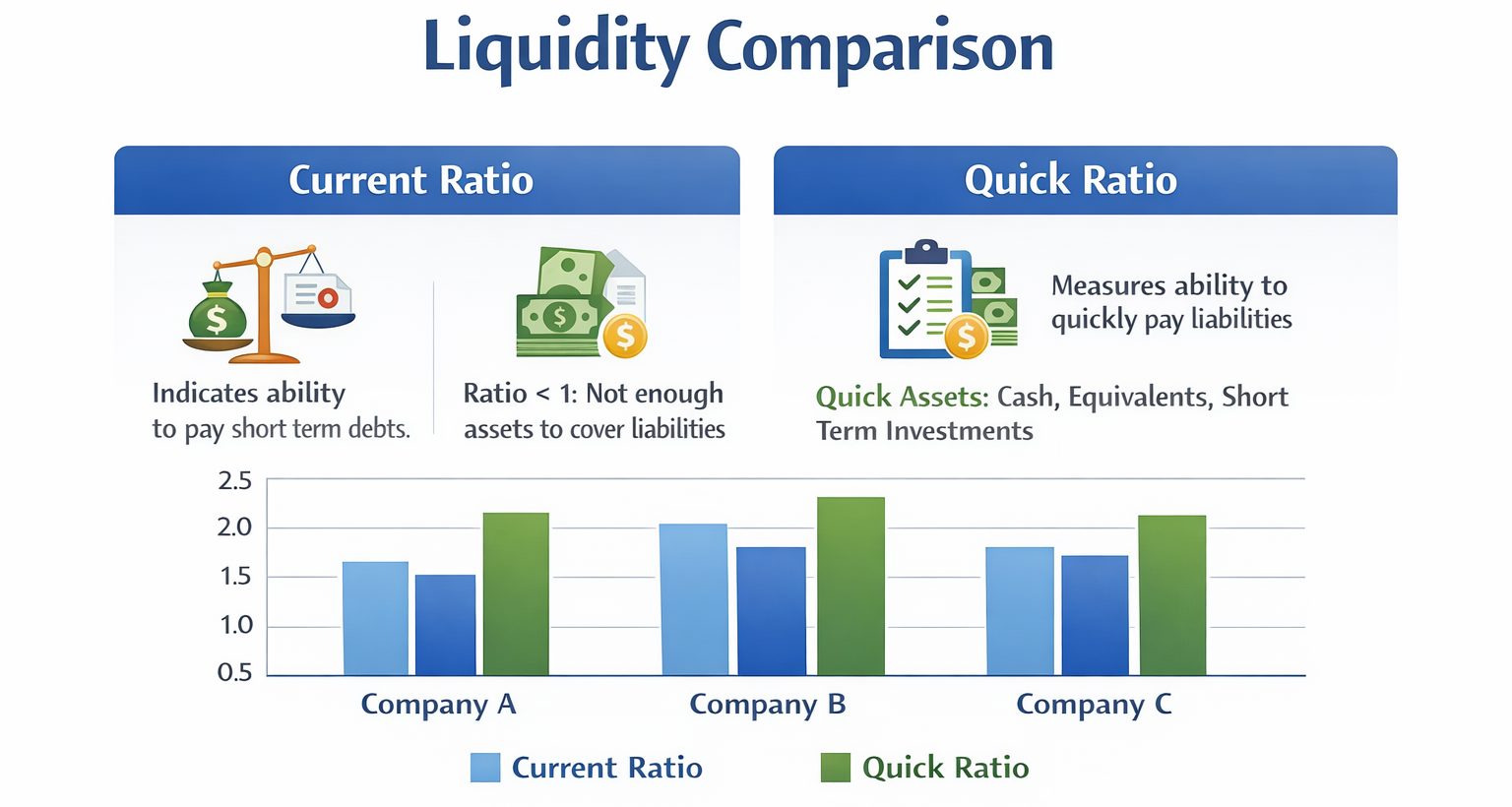

Liquidity Comparison

The following two ratios helps us understand the financial health of comparable selection and the valuation target. Companies with similar liquidity ratios means they may be of similar financial health.

Current Ratio comparison

Current Ratio indicates the ability of a company to pay off its short term debts. It measures how much current assets the company has in proportion to its current liabilities. A ratio of less than 1 means the company doesn’t have enough current assets to pay of its current liabilities.

Quick Ratio comparison

The quick ratio is a measure of the ability of the company to use its most liquid current assets (such as cash, cash equivalents, short term investments) to extinguish its current liabilities immediately. A low quick ratio may not always be a problem since the company may have adequate long-term prospects against which it may be able to access financing options to raise cash as to meet its current obligations. A similar quick ratio across your comparable selections means the companies have a similar cash / assets to current liabilities profile.

Profitability Comparison

The following three ratios helps us understand how profitable the given target is in comparison with your comparable selections.

RoE

RoE indicates the financial performance of the firm. It indicates how many rupees of net income a company generates for every rupee of shareholder equity. Meaning, it is the net income divided by the shareholders equity. Shareholders equity is how much the shareholders of the firm owns after subtracting its liabilities.

RoA

RoA is a measure of how much profit a company is able to generate given its total assets. Its simply net income divided by the total assets. The RoE ratio looks at profitability per unit equity, which is the assets minus the liabilities whereas the RoA ration looks at profitability per unit asset.

Net Profit Margin

Net Profit Margin is simply the net income per unit revenue. The net income is what remains after paying off interests, taxes, operating expenses and dividends to preferred shareholders.

Leverage Comparison

Asset to Equity

The Asset to Equity ratio indicates how much of the assets of the company are funded by its shareholders. Assets can be funded either by Equity or Debt. Meaning, if this ratio is more than one, some of the assets are funded by debt. If the total assets are disproportionately higher than the Equity, it means the company has sourced significant amount of debt to fund its assets. The company has a volatile cash flow, it is considered healthy to have a low Asset to Equity ratio, i.e close to 1. If the company has a history of generating strong cash flows, it may be able to afford to stay highly leveraged.

Debt to Equity

Debt to equity is a measure of the percentage of Debt and Equity funding the firm has on its balance sheet. These two ratios indicate how leveraged a firm is.

Comparable Companies should be similarly leveraged.

Efficiency Comparison

Asset Turnover

Asset turnover indicates how efficiently the company is able to generate sales / revenue on its assets. It is simply total revenue per unit total assets. While using Asset Turnover ratio to compare, you may also want to look at the firms AT ratio trend to ensure the the company’s single year AT ratio is not varying significantly from its past years.

If you’re a valuation professional looking to build defendable valuation models using techniques like DCF or Comparable Company Analysis, feel free to take a tour of SignalX.ai or book a demo. We enable valuation professionals to automate bulk of the data extraction and analysis they do in their projects on a routine basis so that time is instead spent of observation and crafting quality assumptions.