As companies form a network of third-party ecosystems consisting of suppliers, vendors, joint ventures, or subsidiaries, a seamless mutually beneficial strategic business process emerges. This network of alliances reduces costs, provides access to scarce resources and skillsets, and enables experimentation and innovation at a scale that was unfathomable only a few years ago.

That being said, not everything is hunky-dory. There are risks to being reliant on third parties. Legal liability for actions by third parties, regulatory enforcement with punitive fines and reputational damage, and decline in share prices are some that are best avoided.

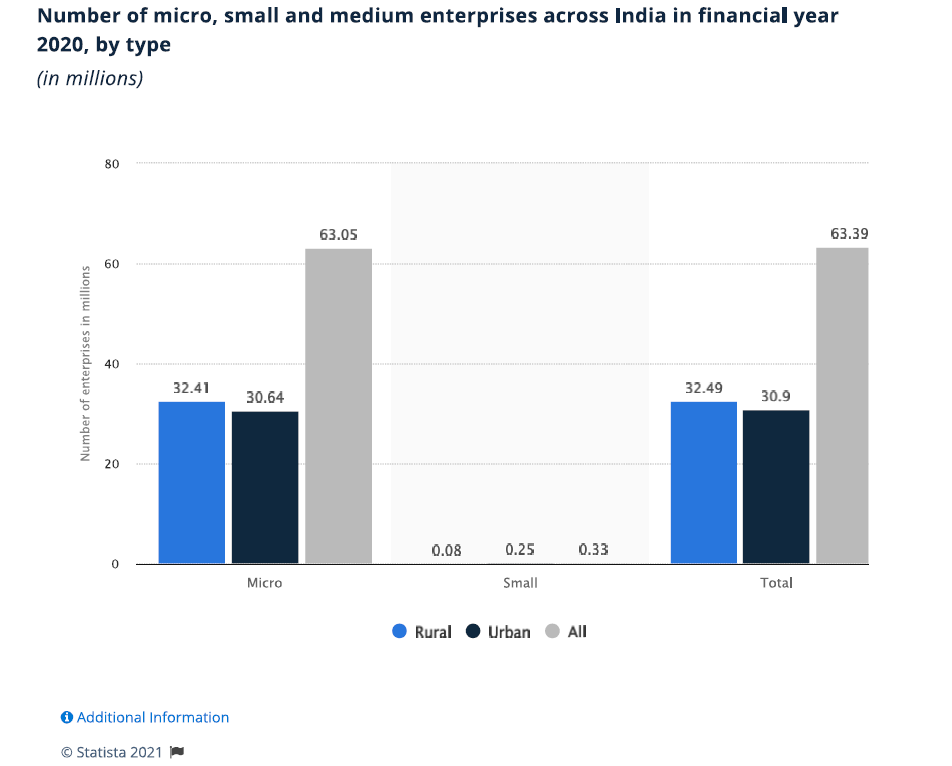

According to Statista, the Indian economy recorded over 63 million micro, small and medium businesses in 2020 – registered and unregistered. To put that in perspective, that’s 95% of the total industrial units in the country.

Yet, a few pertinent questions remain:

Where does your company stand in this complex ecosystem?

How do you navigate the ecosystem?

How do you know who to engage with and who to avoid?

A holistic 360 degree due diligence on a small business process helps you address these questions and arrive at an informed decision while choosing your business partners.

What is Due Diligence on a Small Business?

Due diligence on a small business is a comprehensive assessment that you run to establish the legitimacy of any business target. The aim of this process is to help you determine if the target is in good business standing and has the right assets to support its operations.

It is an essential means to reduce the risk of doing business with a partner possessing a grey business reputation.

Why is Due Diligence on Small Business Important?

Deloitte reports that failure to adequately identify and manage third parties in your supply chain can result in fines and revenue losses to the tune of US$2-50 million. If your company is dealing with a ton of small businesses, it’s important that you take adequate measures to safeguard your business operations and circumvent potential pitfalls taken care by an effective due diligence on a small business.

Running Due Diligence on a Small Business

A Step by Step Guide

Step 1: Identify your objective for conducting due diligence

Once you have identified the business objective, you need to understand the type of small business your target is.

Step 3: Understand the compliance & legal structure

Now that you know the type of business, you can start looking into the legal aspects of the business. You’ll need to understand the legal structure of the business. This includes things like:

Type of business – Sole Proprietor, Partnership, Limited Liability Company, Corporation

Doubtful if your new business partner has the financial wherewithal to take major business leaps with you? Take a comprehensive look at the company’s balance sheet and the profit and loss statement. A balance sheet shows where the business stands financially. The P&L shows how much revenue the business generated during a certain period of time.

Step 5: Evaluate the management team

You also need to evaluate the management team. This involves looking at the people who run the business.

Are they trustworthy?

Do they have a competent professional history?

Do they have any litigation history?

Step 6: Check the company’s website and social media handles

The pandemic has made the internet the most important marketplace, today. A strong business partner will have a well-rounded and informative digital presence. Check the company’s website to see if it provides information about the business. Check whether the company’s social handles respond to queries, requests and customer complaints. This helps you associate with more responsible and responsive business partners.

Step 7: Look for signs of fraud

There are several ways in which businesses commit fraud. Some of these include falsifying records, using fake invoices and money laundering.

A due diligence exercise can help you identify signs of any of these activities and ensure you enter a partnership with no surprises coming your way.

Step 8. Obtain independent advice from experts

You can get expert opinions if you have any doubts about the legitimacy of the business. One option could be to outsource due diligence to Due Diligence experts.

Checklist for Due Diligence on Small Business

What are the Risks Associated with Dealing with Small Businesses?

Compliance Risk

In order to comply with regulations, you must ensure that your business partners’ activities adhere to compliance procedures. Non-compliance may result in fines and penalties that trickle down to impact your business. In addition, failure to comply with regulations could mean that you are not eligible to receive perks.

Production Risk

Small businesses often operate on a shoestring budget. This means that they cannot afford to invest heavily in production processes. This makes them vulnerable to fluctuations in demand and supply.

Fraud Risk

It is easy for fraudsters to infiltrate small businesses because they usually have lesser barriers to entry. A fraudulent business owner may try to steal funds, misrepresent products or services or operate outside the bounds of accepted financial, legal and ethical conduct..

Reputational Risk

Your company’s reputation may be at stake if the small business that engages with you does not perform well. For example, if the business fails to deliver its product or service as promised, it could damage your brand. Your customers’ dissatisfaction might reflect on your company’s performance.

To conclude, performing due diligence on a small business isn’t optional anymore. The multitude of risks associated with engaging with business partners calls for a thorough, timely and data-driven due diligence process that helps you mitigate third party risks. It also paves the way for a strong and lasting relationship with your small-business partners.

FAQs

How should I conduct due diligence on a small business?

There are several ways to carry out due diligence on a small business. You can hire an external investigator, use a third party vendor, or use a combination of both approaches.

Should I get legal counsel when carrying out due diligence on a small business?

Yes. When you engage in due diligence on a small business, you are considering entering into a contract with another individual or entity. Therefore, you should always consult with a lawyer before signing any agreement.

Can I conduct due diligence on a small business myself?

Yes. But you should remember that due diligence on a small business is an important part of the relationship between two parties. Therefore, you should never take shortcuts. Conducting due diligence on a small business yourself could put your company in danger.

What happens after I complete due diligence?

After completing due diligence on a small business, you will receive either a “go” or a “no go” decision. This means that you will either proceed with the deal or reject the opportunity.

Contains information related to marketing campaigns of the user. These are shared with Google AdWords / Google Ads when the Google Ads and Google Analytics accounts are linked together.

90 days

__utma

ID used to identify users and sessions

2 years after last activity

__utmt

Used to monitor number of Google Analytics server requests

10 minutes

__utmb

Used to distinguish new sessions and visits. This cookie is set when the GA.js javascript library is loaded and there is no existing __utmb cookie. The cookie is updated every time data is sent to the Google Analytics server.

30 minutes after last activity

__utmc

Used only with old Urchin versions of Google Analytics and not with GA.js. Was used to distinguish between new sessions and visits at the end of a session.

End of session (browser)

__utmz

Contains information about the traffic source or campaign that directed user to the website. The cookie is set when the GA.js javascript is loaded and updated when data is sent to the Google Anaytics server

6 months after last activity

__utmv

Contains custom information set by the web developer via the _setCustomVar method in Google Analytics. This cookie is updated every time new data is sent to the Google Analytics server.

2 years after last activity

__utmx

Used to determine whether a user is included in an A / B or Multivariate test.

18 months

_ga

ID used to identify users

2 years

_gali

Used by Google Analytics to determine which links on a page are being clicked

30 seconds

_ga_

ID used to identify users

2 years

_gid

ID used to identify users for 24 hours after last activity

24 hours

_gat

Used to monitor number of Google Analytics server requests when using Google Tag Manager

1 minute

Marketing cookies are used to follow visitors to websites. The intention is to show ads that are relevant and engaging to the individual user.

Pinterest Tag is a web analytics service that tracks and reports website traffic.