Why Traditional Vendor Due Diligence Fails to Stop Input Tax Credit (ITC) Fraud

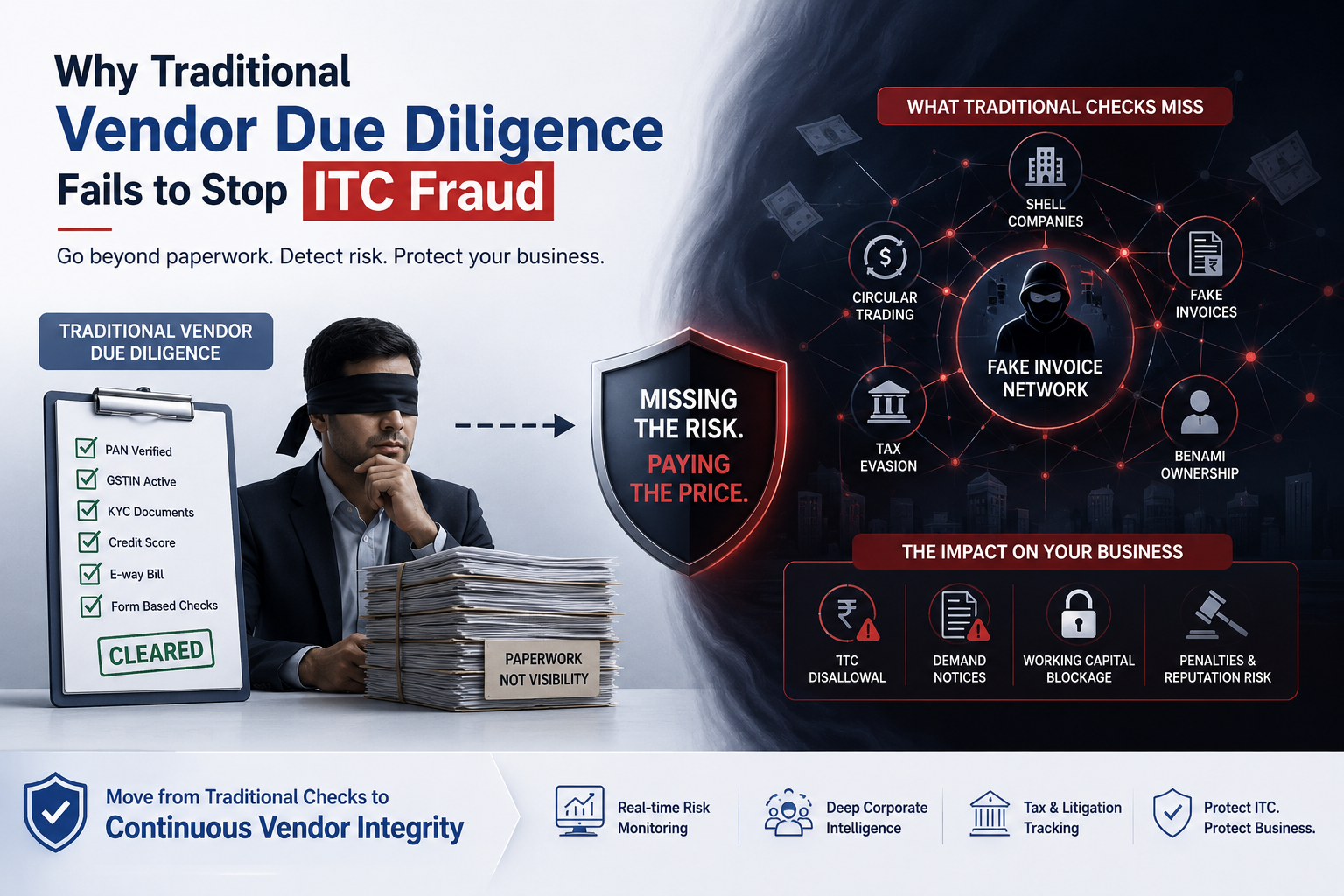

For years, we in the enterprise corporate risk space treated vendor onboarding like an administrative checkpoint. We ran our standard KYC, verified corporate identity, checked basic credit scores, and assumed our supply chain was secure.

But over the past few years, the ground has completely shifted beneath us.

In India’s complex tax ecosystem, a clean PAN card and an active GSTIN are no longer proof of a vendor’s integrity. The alarming rise of sophisticated, multi-layered tax evasion networks has turned Input Tax Credit (ITC) fraud into one of the single largest financial and legal threats to modern enterprises.

When central tax formations under the CBIC detected an astounding ₹58,772 crore in fake ITC fraud across 15,283 cases in FY 2024–25 followed by over 24,109 fake invoice cases detected in just the first seven months of FY 2025–26 it became painfully clear: traditional vendor due diligence is broken.

The harsh reality is that honest businesses are becoming collateral damage. When our suppliers engage in circular trading or fail to deposit taxes, the government doesn’t just go after them they freeze our working capital, deny our ITC claims, and slap us with demand notices.

Here is exactly why traditional vendor screening fails to stop this damage, and how we are fundamentally changing the narrative.

The Core Problem: Why Traditional Vendor Due Diligence is Blind to Tax Fraud

When we look at how traditional Third-Party Risk Management (TPRM) tools operate, they are inherently backward-looking and structurally disconnected from operational realities. They fail to stop ITC fraud for three specific reasons:

1. The “Static Snapshot” Trap

Traditional due diligence relies on point-in-time checks. We verify a supplier in January during onboarding, see that their GST status is “Active,” and give them a green light. However, fraud syndicates often deploy what law enforcement calls “sleeping modules” bogus entities created using compromised or cloned identities that remain entirely dormant to pass initial checks. Upon entering our supply chain, they generate substantial quantities of paper-based, counterfeit invoices without the movement of any genuine goods, disseminating fraudulent Input Tax Credit (ITC) along the way before disappearing entirely.

2. Over-Reliance on Forms Instead of Forensic Substance

Most compliance processes rely heavily on looking at self-certified paperwork or standard IT questionnaires. But a fraudster running an invoice factory can easily hand over clean registration forms, an impressive website, and a valid e-way bill template. What traditional tools fail to analyze are the hidden corporate anomalies. They don’t look at the corporate ecosystem behind the vendor:

-

Are the promoters connected to other struck-off shell companies?

-

Is there an artificial, circular cash flow running through their bank accounts to manufacture fake commercial turnover?

-

Do they actually possess the physical and economic asset capacity to deliver ₹50 crore worth of raw materials?

3. Disconnected Data Silos

Procurement teams use one tool for onboarding, Finance uses another for ERP ledger reconciliation, and Legal monitors independent court filings. Because these systems don’t talk to each other in real time, a critical alert such as a vendor defaulting on consecutive state-level tax filings or facing an active anti-evasion investigation in an out-of-state jurisdiction gets entirely lost in transmission. By the time the mismatch hits our GSTR-2B log, the damage is already done.

Which Vendors Are Quietly Moving from Green to Red?

Most supplier risks emerge long after onboarding.

The Solution: Moving to Continuous Vendor Integrity Automation

To protect working capital and shield companies from aggressive tax enforcement, we had to stop treating vendor verification as an isolated administrative chore and turn it into a continuous, data-driven risk infrastructure.

This is exactly why we built SignalX.ai.

At SignalX, we approached the problem from a corporate governance and forensic standpoint. We acknowledged that in order to completely eradicate supply chain tax risk, businesses require real-time, comprehensive visibility that connects procurement with regulatory compliance.

How SignalX Transforms Vendor Management

Rather than pursuing documents or conducting manual database searches that require weeks, SignalX presents a consolidated, 26-parameter risk scorecard driven by direct-to-source API automation.

-

Forensic Background Screening & UBO Tracking: The moment a new supplier enters the funnel, SignalX instantly crawls over 200 regulatory bodies, the Ministry of Corporate Affairs (MCA), and global AML watchlists. It maps out Ultimate Beneficial Ownership (UBO), flagging if a vendor’s promoters are tied to high-risk shell entities, circular trading rings, or politically exposed networks.

-

Deep Financial and Capacity Analysis: We look past the invoice. SignalX evaluates a vendor’s true financial solvency, active credit defaults, and employee metrics via EPFO data to verify their actual economic capacity to execute contracts, ensuring they aren’t just an “invoice factory” on paper.

-

Continuous Court and Tax Litigation Monitoring: This is where we break away from traditional methods entirely. SignalX continuously tracks active civil, criminal, and tax-related litigations across more than 7,000 Indian court jurisdictions. If an onboarded supplier is suddenly flagged for GST non-compliance, tax evasion, or a retroactively cancelled registration in any part of the country, our continuous monitoring engine surfaces an immediate alert.

Enterprise Benefits: Shifting from Reactive to Protected

By shifting from manual, form-driven checks to SignalX’s automated lifecycle monitoring, enterprises across high-stakes industries like manufacturing, pharmaceuticals, and financial services are transforming how they do business.

| Traditional Due Diligence Process | The SignalX Advantage |

| Onboarding Speeds: Takes 7 to 14 business days of manual review per vendor. | Onboarding Speeds: Complete, audit-ready forensic verification within days rather than weeks. |

| Risk Visibility: Restricted to static KYC documents and basic credit scores. | Risk Visibility: Multidimensional 26-parameter live scorecards tracking operational data. |

| Tax Protection: Reactive; errors are discovered late during tax reconciliations. | Tax Protection: Proactive; real-time alerts block payments to high-risk or non-compliant entities. |

The true business impact goes far beyond avoiding tax penalties. Companies leveraging this infrastructure are experiencing massive operational advantages:

-

Shielding Working Capital: By catching high-risk tax anomalies early, finance teams can confidently halt payments or withhold taxes before capital is locked up by provisional attachment orders or blocked ITCs.

-

Seamless ERP Integration: SignalX hooks directly into enterprise ERP environments like SAP, Oracle, and ServiceNow via automated APIs. This means a vendor’s risk profile dynamically alters their payment and purchase order eligibility within the company’s core operational system automatically.

-

Total Peace of Mind: Procurement and compliance teams no longer have to live in fear of sudden tax raids, bank account freezes, or department notices stemming from unverified supplier behavior.

We can no longer afford to let the vulnerabilities of our suppliers dictate our corporate security. To build a genuinely resilient enterprise, we must demand absolute visibility into the corporate integrity of our entire supply chain from critical tier-one partners down to long-tail regional vendors. With continuous, automated risk intelligence, we finally have the power to do exactly that.

What Could Your Team Achieve If Vendor Risk Management Ran on Autopilot?

For a deeper look into how modern enforcement agencies use technology-driven analytics to identify these exact supply chain anomalies, you can review this detailed breakdown of recent tax enforcement actions in India, which highlights the massive scale of invoice circulation networks and provides vital context on why real-time corporate monitoring has become an operational necessity for businesses today.